Engine (Backtest)

Phase-by-phase research history, walk-forward, slippage stress.

What does /engine do?

The Engine is the research lab. It runs historical backtests of individual strategy sleeves (Donchian breakouts, EMA crosses, momentum, mean-reversion, vol-spike shorts, commodity sleeves on XAU/XAG, etc.) over 5 years of price data and validates them with a rolling walk-forward harness.

You can stress-test any sleeve at 0/5/10/20 bps slippage to see if its edge survives realistic trading costs.

Walk-Forward (WF) — the real test

Single-period backtests are easy to curve-fit. Walk-forward is honest: - Rolling 180-day train → 30-day test windows over 5 years of history - Each window re-ranks the catalog by train-period Sharpe - Top-5 sleeves get Sharpe-weighted allocation (Phase 37), with greedy decorrelation (max pairwise corr 0.7) - Returns are concatenated only from the out-of-sample test periods

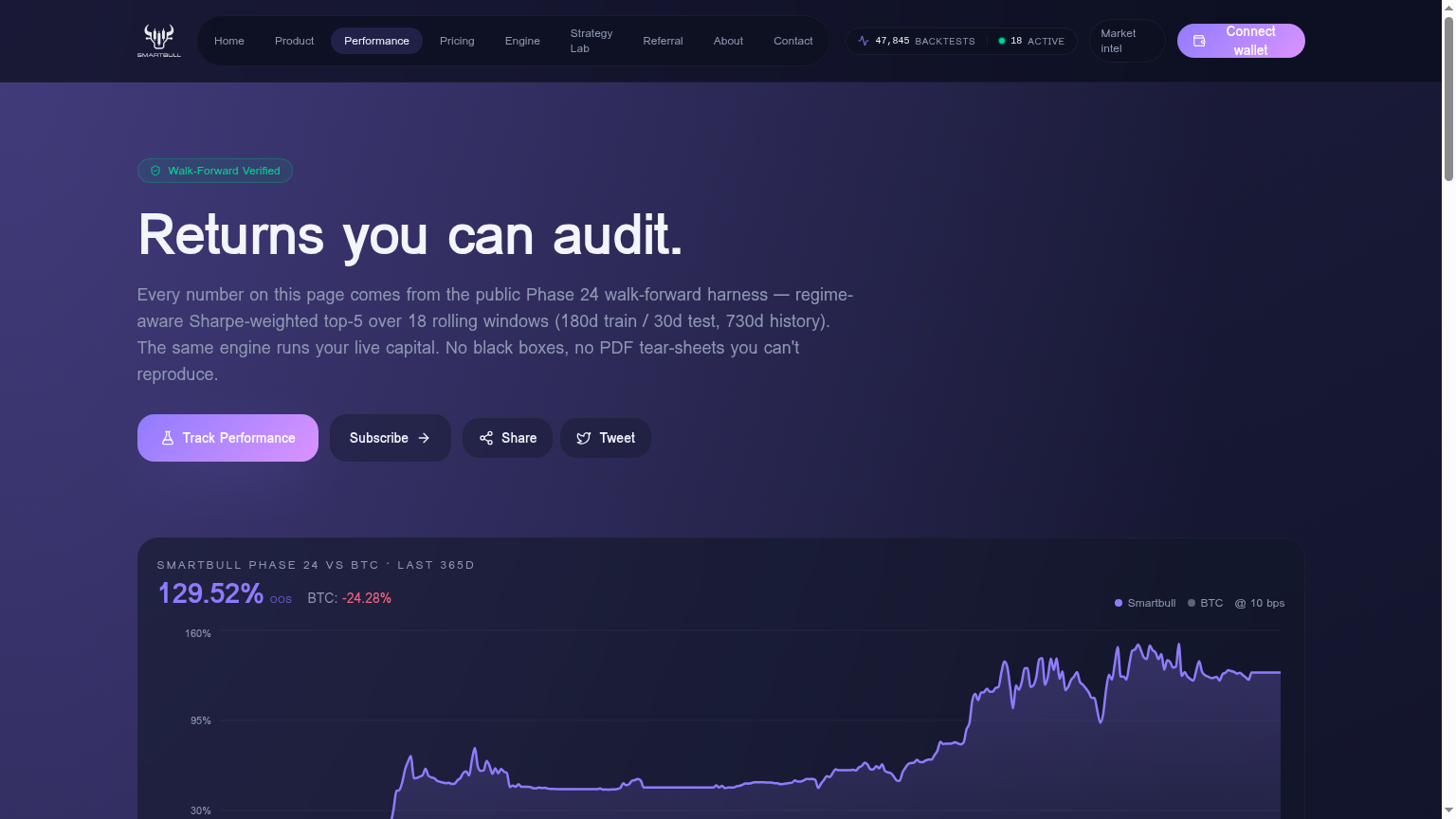

This is what we trade live. Current WF baseline: +163.33% last-12m at 10 bps, Sharpe 3.31, 78 windows (Phase 37, May 17 2026). Realistic live target: +110-140% over 18 months at 5-8 bps actual slippage.

Phases 4 → 24 — what changed

We publish every iteration so you can audit the research: - Phase 4 — baseline (Donchian-20 + BTC regime + run-winners) - Phase 11 — pyramid into winners (+1R add, breakeven stop) → ~75% ceiling - Phase 15 — short-only vol-spike crash sleeve (uncorrelated) - Phase 17 — walk-forward harness shipped - Phase 18 — slippage stress test (0/5/10/20 bps) - Phase 19 — low-turnover sleeves + XAU/XAG commodities - Phase 20 — WF history extended to 730 days - Phase 37 — Regime-aware Sharpe-weighted top-5 + greedy decorrelation (current live) - Phase 25 — history extended to 5y (covers 2021 bull, 2022 bear, 2023 chop, 2024–25)

Reverted (don't ask us to bring them back): Phase 6 (funding gate + vol-target), Phase 8 (weekend+ATR combo), Phase 10, 12, 13, 14, 22.